| Company | Value | Change | %Change |

|---|

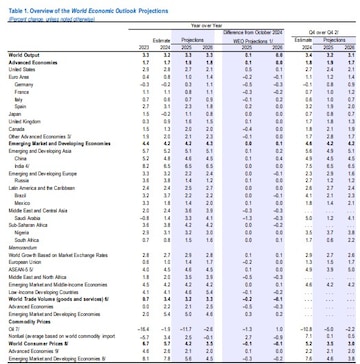

In India, growth is projected to be solid at 6.5 percent in FY26 and FY27, as projected in October and in line with potential, the IMF said in its report. India’s growth projections are 6.8 percent for 2025 and 6.5 percent for 2026 based on calendar year.

“Global growth is expected to remain stable, albeit lackluster. At 3.3 percent in both 2025 and 2026, the forecasts for growth are below the historical (2000–19) average of 3.7 percent and broadly unchanged from October. The overall picture, however, hides divergent paths across economies and a precarious global growth profile,” the IMF said in its latest report.

Advanced economies’ growth is projected at 1.9% in 2025, 10 basis points higher than the October WEO forecast, and at 1.8% in 2026. The Emerging Market & Developing Economies (EMDEs) growth, on the other hand, is projected at 4.2% in 2025, unchanged from the October WEO, and at 4.3% in 2026, which is 10 basis points higher than the October WEO forecast.

Among advanced economies, growth forecast revisions go in different directions. In the United States, the IMF said underlying demand remains robust, reflecting strong wealth effects, a less restrictive monetary policy stance, and supportive financial conditions. Growth is projected to be at 2.7 percent in 2025. This is 0.5 percentage point higher than the October forecast, in part reflecting carryover from 2024 as well as robust labor markets and accelerating investment, among other signs of strength, the report added. Growth is expected to taper to potential in 2026.

In the euro area, IMF said growth is expected to pick up but at a more gradual pace than anticipated in October, with geopolitical tensions continuing to weigh on sentiment. Weaker-than-expected momentum at the end of 2024, especially in manufacturing, and heightened political and policy uncertainty explain a downward revision of 0.2 percentage point to 1.0 percent in 2025, it said. In 2026, IMF added, growth is set to rise to 1.4 percent, helped by stronger domestic demand, as financial conditions loosen, confidence improves, and uncertainty recedes somewhat.

In emerging market and developing economies, growth performance in 2025 and 2026 is expected to broadly match that in 2024. With respect to the projection in October, growth in 2025 for China is marginally revised upward by 0.1 percentage point to 4.6 percent.

Global headline inflation is expected to decline to 4.2 percent in 2025 and to 3.5 percent in 2026, converging back to target earlier in advanced economies than in emerging market and developing economies, the report said.

“Some divergence between large economies has been cyclical, with the US economy operating above its potential while Europe and China are below. Under current policies, this cyclical divergence will dissipate. But the divergence between the US and Europe is more due to structural factors, and the disconnect will linger if these are left unaddressed. It reflects persistently stronger US productivity growth, particularly but not exclusively in the technology sector, linked to a more favourable business environment and deeper capital markets. Over time, this translates into higher returns on US investment, increased inbound capital flows, a stronger dollar and US living standards pulling away from those of other advanced economies,” Pierre-Olivier Gourinchas, Chief Economist at the IMF said in a blog.

The IMF said it had refrained from making assumptions about potential policy changes that are currently under public debate, while adding that economic policy uncertainty was elevated with the newly elected governments in 2024.

“While many of the policy shifts under the incoming US administration are hard to quantify precisely, they are likely to push inflation higher in the near term relative to our baseline. Some indicated policies, such as looser fiscal policy or deregulation efforts, would stimulate aggregate demand and increase inflation in the near term, as spending and investment increase immediately. Other policies, such as higher taris or immigration curbs, will play out like negative supply shocks, reducing output and adding to price pressures,” Gourinchas said.

Gourinchas added that a combination of surging demand and shrinking supply would likely reignite US price pressures, though the effect on economic output in the near term would be ambiguous. “Higher inflation would prevent the Federal Reserve from cutting interest rates and could even require rate hikes that would in turn strengthen the dollar and widen US external deficits. The combination of tighter US monetary policy and a stronger dollar would tighten financial conditions, especially for emerging markets and developing economies. Investors already anticipate such an outcome, with the US dollar gaining around 4 percent since the November election.”

The economic outlook report said that medium-term risks to the baseline growth projections were tilted to the downside, while the near-term outlook was characterized by divergent risks. Upside risks could lift already-robust growth in the United States in the short run, whereas risks in other countries are on the downside amid elevated policy uncertainty, it said.

Policy-generated disruptions to the ongoing disinflation process could interrupt the pivot to easing monetary policy, with implications for fiscal sustainability and financial stability. Managing these risks requires a keen policy focus on balancing trade-offs between inflation and real activity, rebuilding buffers, and lifting medium-term growth prospects through stepped-up structural reforms as well as stronger multilateral rules and cooperation, the report added.

“Monetary policy should ensure that price stability is restored while supporting activity and employment. In economies in which inflationary pressures are proving persistent and the risk of upside surprises is on the rise, a restrictive stance will need to be maintained until evidence is clearer that the underlying inflation is sustainably returning to target,” said the report, adding that in economies in which activity is cooling fast and inflation is on track to durably go back to target, a less restrictive stance is justified.

The IMF also said that fiscal policy should consolidate to put public debt on a sustainable path and restore the space needed for more agile responses. The consolidation path needs to be carefully calibrated to the conditions a particular economy is facing. It should be sizable yet gradual to avoid hurting economic activity, clearly communicated to avoid disruptions in debt markets, and credible to achieve long-lasting results. Adopting a growth-friendly approach and mitigating the adverse impacts on poor individuals could help preserve the economy’s potential and maintain public support, the IMF advocated in its suggestions for policy priorities.