SACRAMENTO — As more people in California lose private insurance, the state’s FAIR plan is filling up with homes in places the industry itself has classified as low-risk for wildfire.

The state regulator has a strategy that they say will help people get off the FAIR plan. A CBS News California analysis reveals the state’s solution might not be enough.

For Ken Cavalli and Lisa Fine-Cavalli, their new home in West Roseville is their dream home. It’s about halfway between Sacramento and the Sierra Nevada foothills. Down their street, flat open fields are filling in with new housing developments without a tree in sight.

They needed more space for their blended family, so they decided to buy one of those new homes, just a few minutes away from their current home and in the same ZIP code.

“I thought it was going to be simple,” Lisa said, “that our insurance was just going to transfer over.”

But it didn’t. When the Cavallis applied for a new policy with their same insurer, they were denied.

“I thought, ‘Are you kidding me?’ ” Lisa said. “Ken’s been on their insurance for 30 years, and we’ve never had any problems. We never had any claims.”

They asked that we not publicly identify their insurer; however, CBS News California learned that their insurer was among several major insurers that had stopped writing new policies in California. When the Cavallis called other companies, they heard the same thing.

The problem is doubled for the Cavallis because it means not only are they without good options for their home, but the buyers of their old home won’t be able to find a plan either.

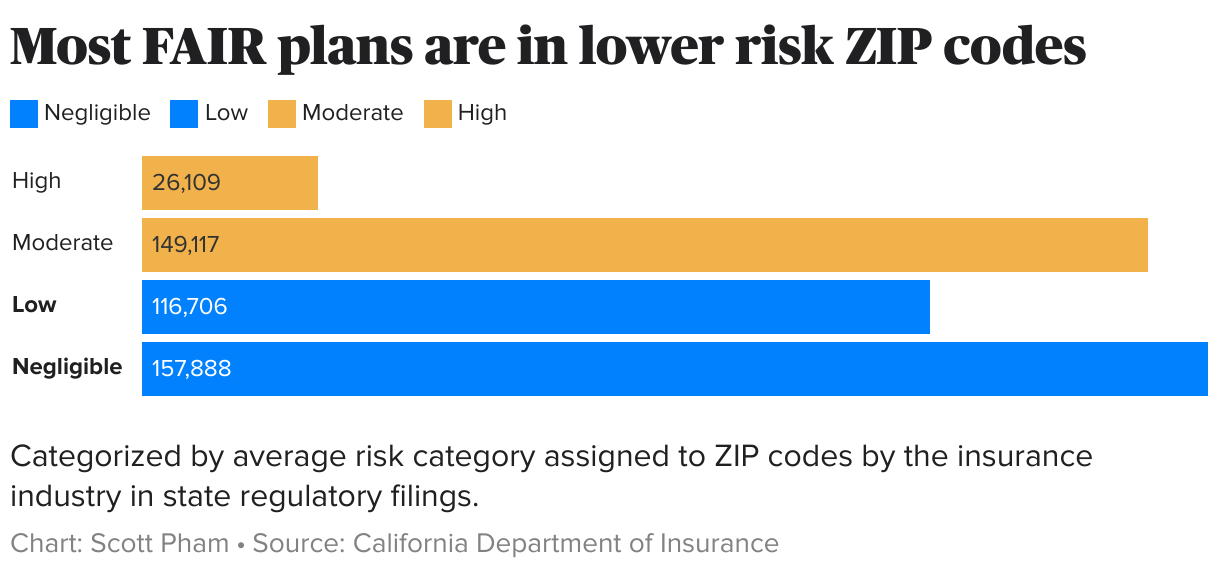

According to wildfire reporting mandated by the state regulator, the industry gave Ken and Lisa’s ZIP code an average risk class of “negligible.” Yet, like nearly half a million other Californians, the Cavallis have found themselves facing a choice between a risky, unregulated out-of-state insurer or the California FAIR Plan, the low-coverage insurer of last resort.

A CBS News data analysis shows that more and more homes in low-risk areas are being forced into the FAIR plan. When using the industry’s own wildfire risk reporting, there are 10 times as many homes in ZIP codes with risk levels in the lowest categories than in the highest.

The FAIR plan is a privately run but state-mandated insurance plan of last resort for those who can’t get homeowners insurance elsewhere. In recent years, this once-small plan has ballooned into one of the state’s largest insurers as more and more Californians find themselves with no other options. About 30 other states have similar programs.

When they’re small and relatively obscure, FAIR plans perform an important function in ensuring the state’s riskiest homes still have some insurance option. But a large FAIR plan is a dangerous liability, as California found out last January. The Los Angeles wildfires quickly drained the plan’s surplus funds, leading to a $1 billion assessment on the rest of the state’s insurers, at least half of which will be passed on to the people with regular insurance polices.

“A canary in the coal mine”

By and large, the insurance industry would rather see a smaller FAIR plan as well, despite contributing to its size by writing fewer policies and announcing bulk “non-renewals” of existing customers.

Rex Frazier, president of an insurance advocacy organization, calls the FAIR plan’s size “a canary in the coal mine,” indicative of larger problems in the market.

“Insurers are not renewing policies,” Frazier said. Because we have a system that has not allowed companies to earn enough money to do business everywhere.”

Frazier said that home insurance rates are objectively underpriced in California, a point of view that’s become increasingly mainstream even if leaders are loath to say it out loud. In national comparisons, Florida and New York have the highest premiums, while California ranks much further down at 20th place below Kansas and Wyoming.

Karl Sussman, a broker in Los Angeles, said that the real reason why people in low-risk places end up on the FAIR plan is a lack of competition.

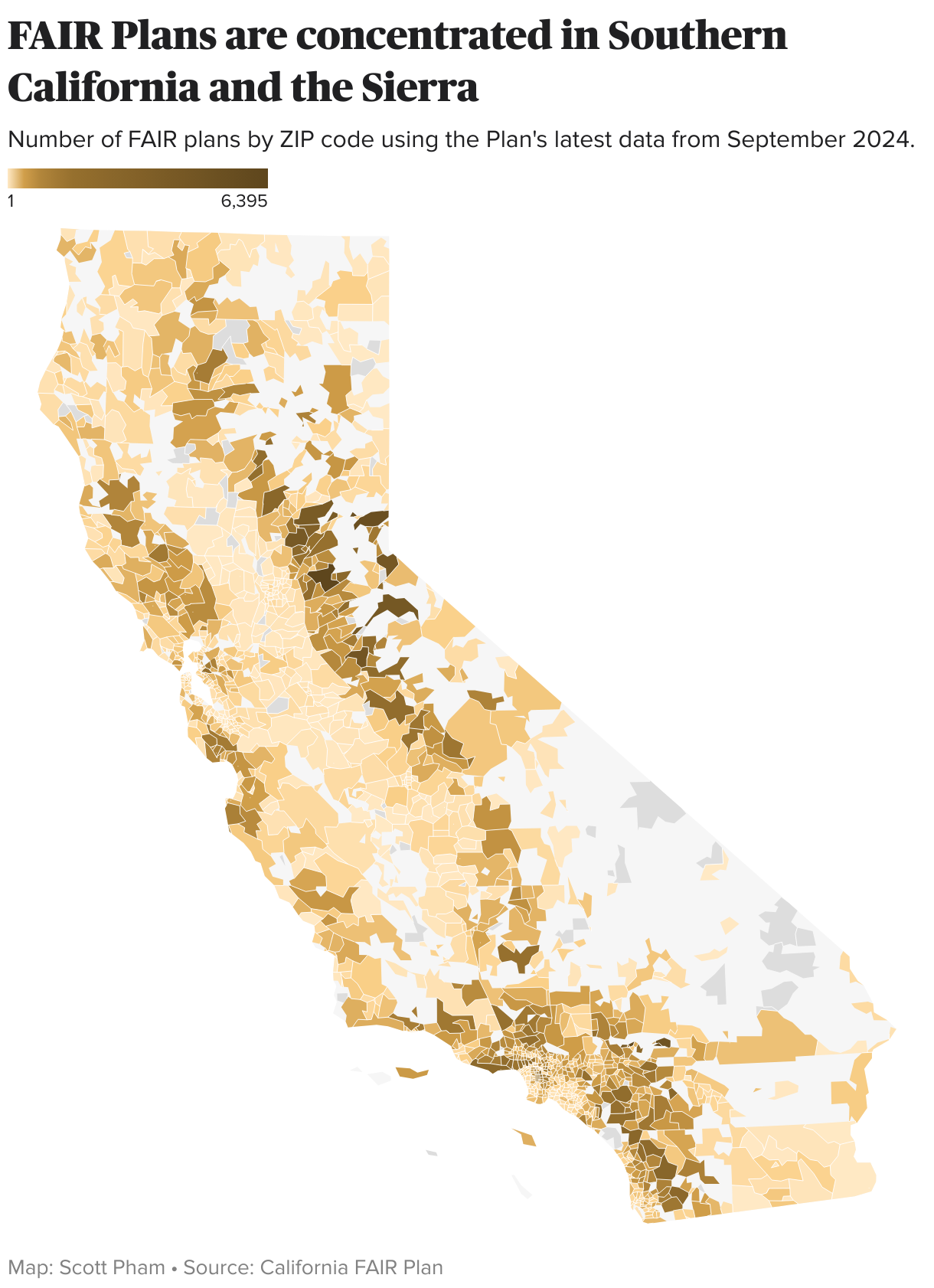

“We’re suffering from that in a major way right now because of the shortage of availability in California,” he said. “This is why we keep seeing the FAIR plan growing and growing and growing. And if you look at the growth, you can see that the majority of the growth is not in the brush. It’s in areas that every carrier should be comfortable writing in.”

He said the FAIR plan won’t start to shrink until insurers start expanding and writing new plans. And they won’t do that, he said, until they can get the higher rates they say they need.

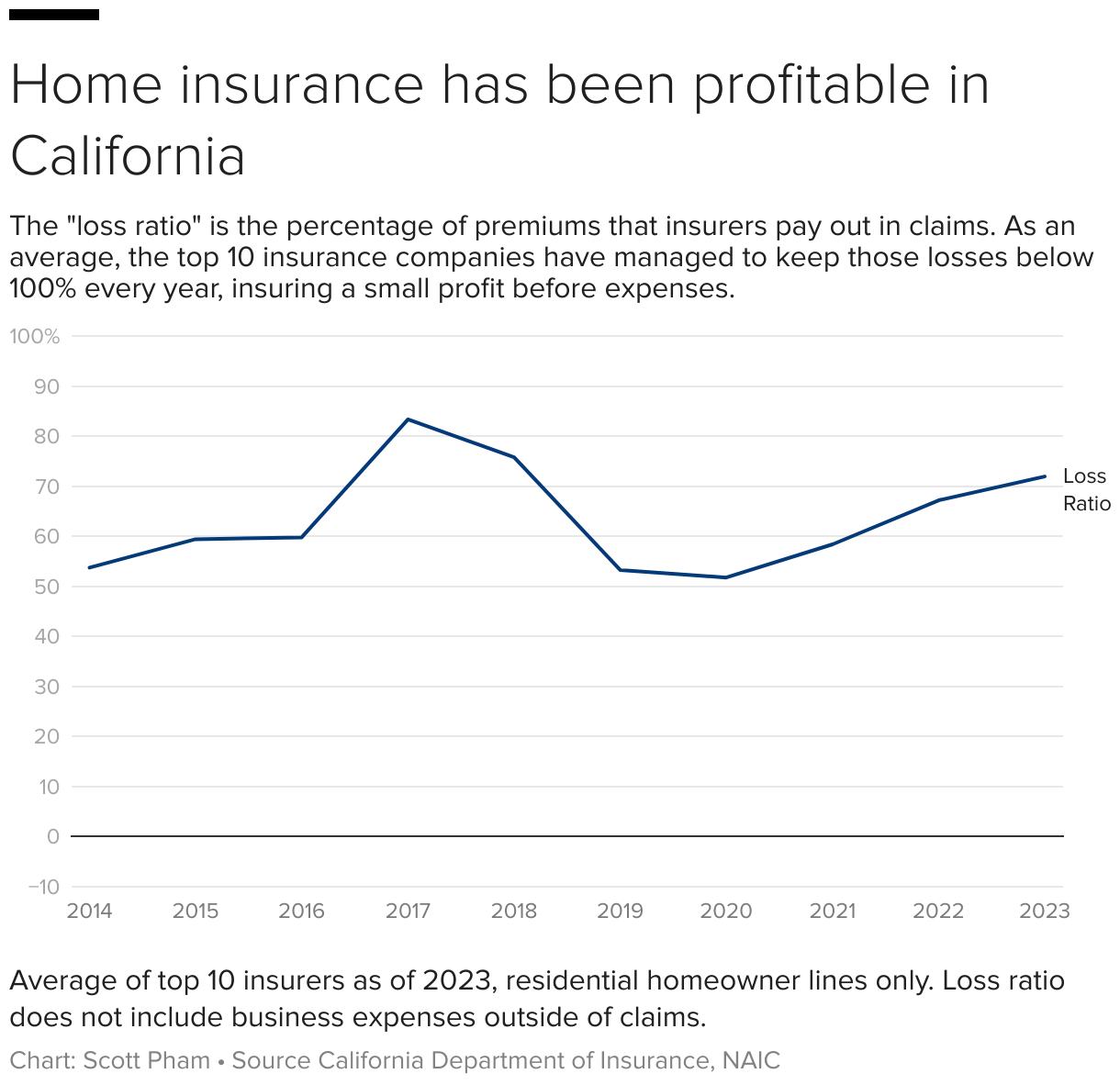

Financial disclosures from the industry show that before expenses, home insurance remains profitable in California on average. Companies consistently report that they take in more premiums than they pay out in claims before other expenses.

Yet, insurers argue profits have been declining, which can hit the large cash reserves they keep to prepare for large disasters. For example, State Farm, the state’s largest insurer, saw its reserves drop from $4 billion in 2016 to an estimated $1 billion last year. The company has reported that the L.A. fires will cost it more than $600 million after its own reinsurance kicks in.

A plan for sustainability

The state’s “sustainable insurance strategy” aims to reduce the FAIR plan’s roster by forcing private insurers to take on more customers in high-risk parts of the state in exchange for other concessions, including one that allows companies to use new models in their rate filings and one that lets them pass on part of the cost of FAIR plan assessments to customers.

The tricky part is that there are a lot of ways to define “high-risk.”

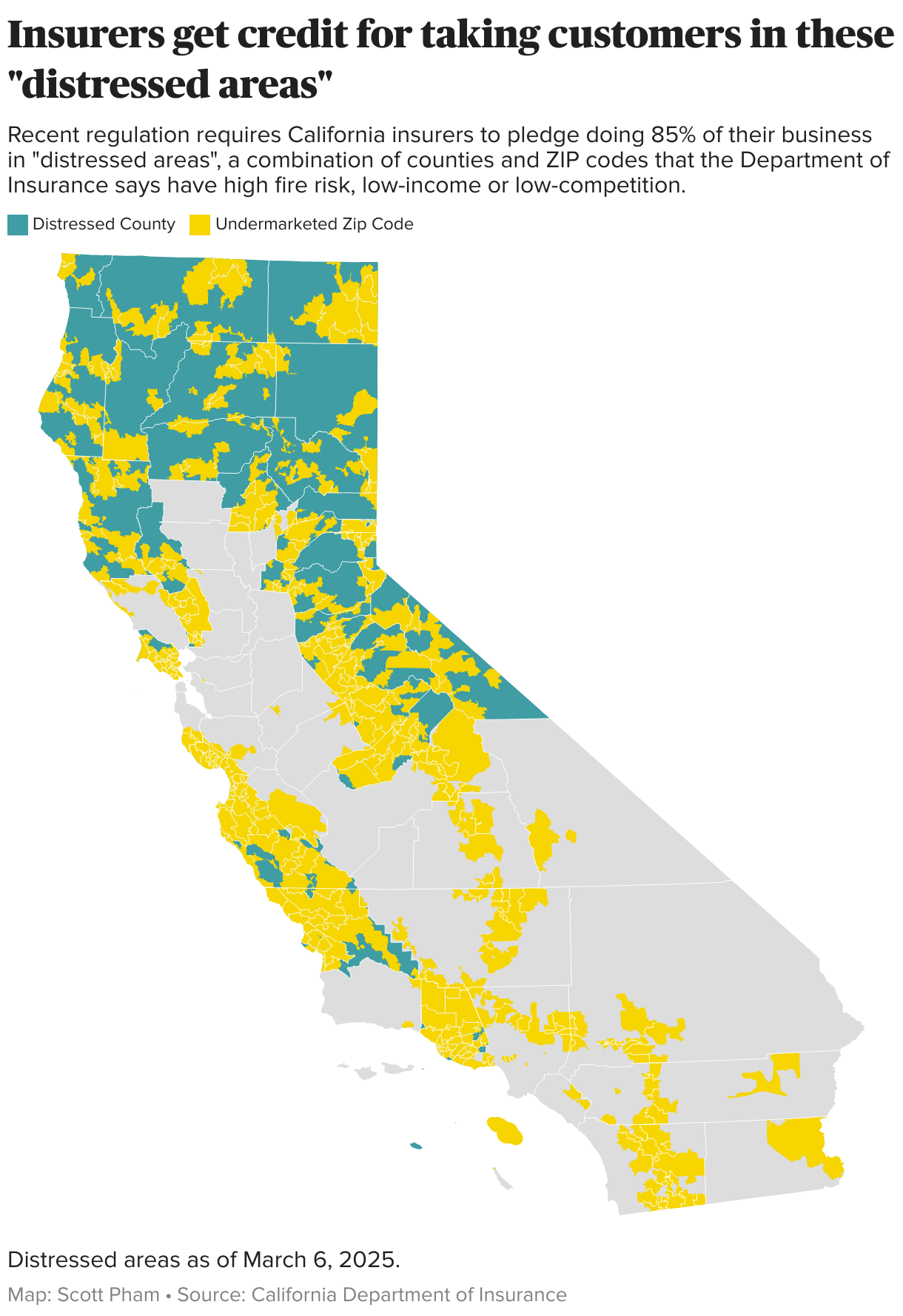

The strategy includes a pledge by insurers to eventually have 85% of their business in so-called “distressed areas,” but it’s not so simple as, say, including all FAIR plans or all high-risk homes. It’s a complex combination of counties, ZIP codes, and individual homes that are included for slightly different reasons.

Here are the ways a plan can qualify as part of that 85%:

1. High-risk FAIR plans

If a home was previously on the FAIR plan and is also considered high-risk by the insurer’s own rating, then that insurer can take that customer and it qualifies as part of the 85%. However, this depends on the insurer’s own individual risk assessment, not a wildfire risk map or anything else. Given that most homes in the FAIR plan are currently in lower-risk ZIP codes, it’s not clear how much this provision would help.

Customers don’t typically know their exact risk, but recent regulations now entitle Californians to receive their risk score from their insurer anytime they apply for a policy or on request after performing some kind of fire mitigation. The California Department of Insurance has details here.

2. Counties with lots of high-risk homes

If a county has more homes rated at high or very high wildfire risk than the median county in the state, then all homes in that county count as part of the 85%. Notably, an insurer can take any home in that county as a customer, they don’t have to be high risk or on the FARI Plan, and count it toward the 85%. The specific counties can change over time, but the Department of Insurance periodically releases a list.

3. High-fire-hazard ZIP codes with deep FAIR plan penetration

This one might be the most confusing of the three. These are ZIP codes in a high- or very-high-fire-hazard region, as reported by Cal Fire’s latest maps. But to officially be a “distressed area,” at least 15% of the homes in the ZIP code must also currently be on the FAIR plan.

Like with the distressed county regulation, the customer doesn’t have to actually be on the FAIR plan to count toward the regulation’s targets.

Put together, the distressed areas look something like this, with many parts overlapping:

The areas cover most of Northern California and the Sierra Nevada, but many existing FAIR plans are concentrated in the Los Angeles area, which the state’s plan largely misses. About 47%, or 200,000 FAIR plan policies, aren’t part of the current distressed areas, and insurers have few incentives to take them back on as customers if they aren’t classified as high-risk.

Notably, neither Palisades nor Altadena were classified as distressed areas under the regulations, and in the “distressed counties” of the north, insurers can get credit for writing any new policies in those counties, whether or not the home was on the FAIR plan or was even high-risk.

What’s best for the whole

Ken Cavalli works in the California State Capitol and is a freelance news photographer for CBS Sacramento, so he and Lisa know a little more than most about how politics works.

“We need to figure out how all these leaders and insurance companies are going to come together and say, ‘OK, this is what’s best for the whole right now,’ ” Lisa said. “Because the nation is in crisis right now, and we’re all aware of it. And now we need to have a way to make sure that families have homes.”